Chris Thompson | Head of Research | Ubika Research | Chris@UbikaResearch.com | 1 (416) 574-0469

Patrick Smith | Analyst | Ubika Research | Patrick@UbikaResearch.com | 1 (647) 444-5506

Maxim Medvedev | Associate | Ubika Research | Max@UbikaResearch.com | 1 (647) 936-6692

William Xiao | Associate | Ubika Research | William.x@gicpartners.com | 1 (647) 828-4632

Gold stocks fall, though, on the back of a stronger U.S. dollar

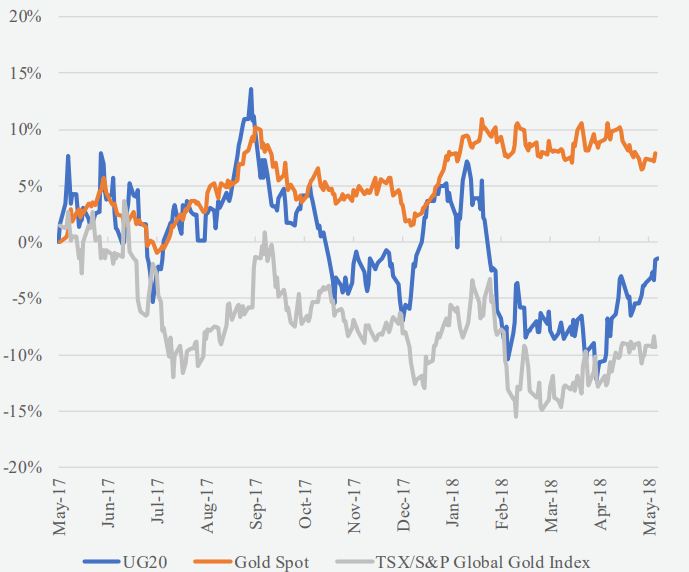

Ubika Gold 20 March 26, 2018 - May 11, 2018

UG20: 5.4% (-1.5% Y/Y)

Gold Price: -2.6% (7.6% Y/Y)

TSX Gold Index: 5.0% (-9.1% Y/Y)

Dollar amounts in CAD unless otherwise stated

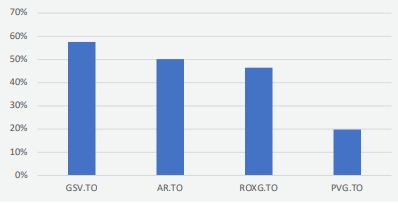

Top Volume Gainers (m/m)

Note: All figures use price close on May 11, 2018.

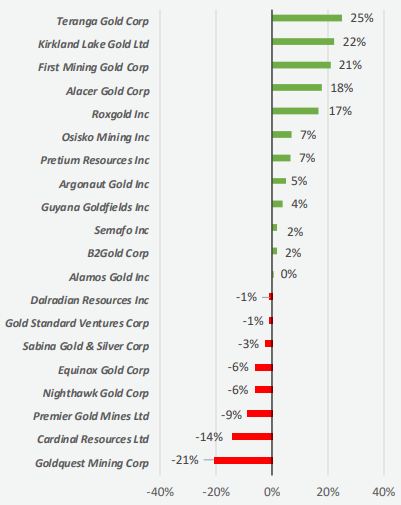

Note: All figures use price close on May 11, 2018.The Ubika Gold 20 Index has increased 5.4% since our last report dated March 26, 2018, exceeding its benchmarks, the Gold Spot price and the Global Gold Index, which decreased 2.6% and increased 5.0%, respectively. Notable performers for this report include:

- Kirkland Lake Gold (TSX:KL), which climbed 22% due to strong exploration results and a positive Q1 2018 performance

- Alacer Gold Corp. (TSX:ASR), which rose 18% due to a positive Q1 2018 performance and near completion of its mine development

- Premier Gold Mines Ltd. (TSX:PG), which slipped 9% due to a negative Q4 2017 and lowered 2018 guidance

Industry Highlights

- This quarter, worldwide demand for gold is the weakest since the 2008 financial crisis. The record low demand can be attributed to the U.S. Federal Reserve raising interest rates. The Fed is anticipating raising the interest rate two more times in 2018, and three additional times in 2019. This should drive investment towards the fixed income market due to higher yields, which may result in further reduction in the demand for gold.

- The US Dollar Index (DXY) hits its peak this year, followed by a drop in gold prices. The U.S. dollar is at its strongest it has been this year, resulting in gold prices breaking its three-day positive streak on May 4.

- Gold prices peaked at US$1,365/oz on April 11 and have declined since. Prices fell to US$1,302/oz on May 1 and in the past week have been rising to US$1,319/oz.

Upcoming Events:

International Mining Investment Conference – May 15 – 16, 2018. The Conference is held in Vancouver, British Columbia, where more than 35 experts throughout the world will discuss strategies and the outlook of the junior mining market.

The Canadian Mining Expo – June 6 – 7, 2018. The Expo is in Timmins, Ontario, and it is considered the largest gold mining show in Canada. The Expo hosts over 300 exhibitors as well as regional and international industry experts.

UG20: Performance Vs. Benchmarks Y/Y

UG20: Performance Distribution

Notable Performers

Kirkland Lake Gold (TSX:KL)

Kirkland Lake Gold is a mid-tier gold producer operating four mines and three milling facilities located in Canada and Australia. The Company’s stock has gained 22% since our last report date, due to its successful drilling results and strong Q1 2018.

Kirkland Lake Gold’s largest producing mine is the Fosterville Mine, located in Australia, which is the largest gold producer in the state of Victoria. It is their largest mine, with a 2018 production guidance of 260,000 – 300,000 oz Au. The Company obtained the mine in 2016 through its acquisition of Newmarket Gold. The mine has been operating since 2005, and high-grade, visible-gold bearing mineralization was discovered in 2015. Once in production, this discovery significantly improved the mine’s overall mineral reserve grade, production profile and unit cost performance.

Kirkland Lake Gold’s largest Canadian asset is the Macassa Mine, located in Kirkland Lake, which has been operating since 1993. The mine has 2018 production guidance of 215,000 – 225,000 oz Au. In January 2018, the Company announced plans to incorporate a new shaft at the mine. This development is necessary for the Company to attain its 400,000 oz Au/year goal. The shaft should support higher levels of production and lower their unit costs.

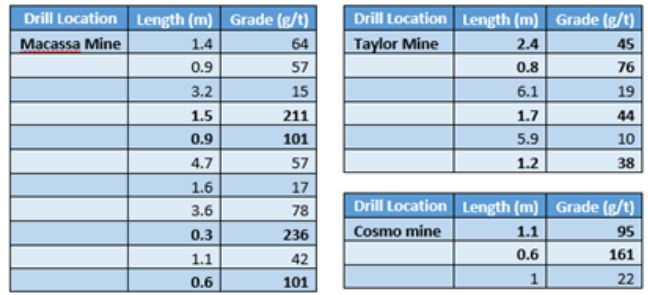

The Company’s Cosmo mine is in the Northern Territory, Australia. The mine had its production suspended mid-2017 to focus on exploration and definition of a gold deposit in the area. The recent test results of the Lantern Deposit expanded the deposit footprint and reported the highest gold grade at Cosmo at 4,750 g/t Au over 0.31m.

The Company had an outstanding 2017 performance, exceeding production guidance. KL was up 174.5% by the end of 2017, while the GDX index rose 5.7%. Below is the summary of Kirkland Lake Gold’s Performance in 2017:

Figure 1 & 2. Kirkland Lake Gold 2017 Performance versus Guidance

Source: Company Presentation

Source: Company PresentationThe Company’s production guidance for 2018 is 620,000 oz Au. In Q1 2018, KL had a record production of 54,000 oz Au at its Macassa mine, totaling production of 148,000 oz Au, which is in line with its production plan. The all-in sustaining costs guidance (AISC) for 2018 is US$750-$800.

Below are the highlights of the drilling results released by the Company from April 25 to May 1. In that period the stock appreciated 12.1%.

Figure 3. Kirkland Lake Gold 2018 Drilling Results

Source: Company News Release

Source: Company News ReleaseBelow are the highlights of the drilling results released by the Company from April 25 to May 1. In that period the stock appreciated 12.1%.

On May 2, the Company released its Q1 2018 results and increased its paid quarterly dividend from $0.02 to $0.03/share. Cash flow per share equated to $1.80 and cash increased by 19% from the previous quarter, amounting to $291M. KL’s price has since increased by 8.3%.

The Company has an average target price of $27.53, representing an 11% upside. The Company has 10 Buy ratings, 1 Hold ratings, and no Sell ratings.

Alacer Gold Corp. (TSX:ASR)

Alacer Gold is a gold producer operating in Turkey. The Company’s stock climed 18% since our last report date, due to strong Q1 2018 performance and its nearly complete expansion project.

Alacer Gold has an 80% interest in the Çöpler Gold Mine located in the Erzincan Province of Turkey, with the remaining 20% owned by their strategic partner, Lidya Mining. The mine is an open-pit, heap leach operation that has been producing gold from oxide ore since 2011. In 2017, the mine produced 168,000 oz Au and had an AISC of US$686/oz.

In 2014, a Feasibility Study revealed that gold production through pressure oxidization of sulfide ore provided the best returns. This method of extraction consists of oxidizing the sulfide minerals at a high temperature and pressure, which releases the trapped gold. Pressure oxidation has a higher gold recovery rate than roasting, one of the most common gold extraction practices, by roughly 10%. In May 2016, Alacer began its Çöpler Sulfide Expansion Project. The expansion project is expected to have its first gold pour in Q3 2018. The Çöpler Sulfide Expansion Project is currently advanced under budget (US$39M in CAPEX savings incurred) with a potential of US$30M in additional savings upon completion. The project has a 2018 production guidance of 50,000 – 100,000 oz Au and is expected to repay itself within three years.

Alacer Gold, leveraging its Çöpler Gold Mine infrastructure, is currently developing the Çakmaktepe Project. It is a heap-leach operation, which is expected to commence operation in Q4 2018 and is expected to contribute 50,000 oz Au in 2019. The 2018 production guidance for Çakmaktepe and Çöpler mine is 70,000 – 90,000 oz Au.

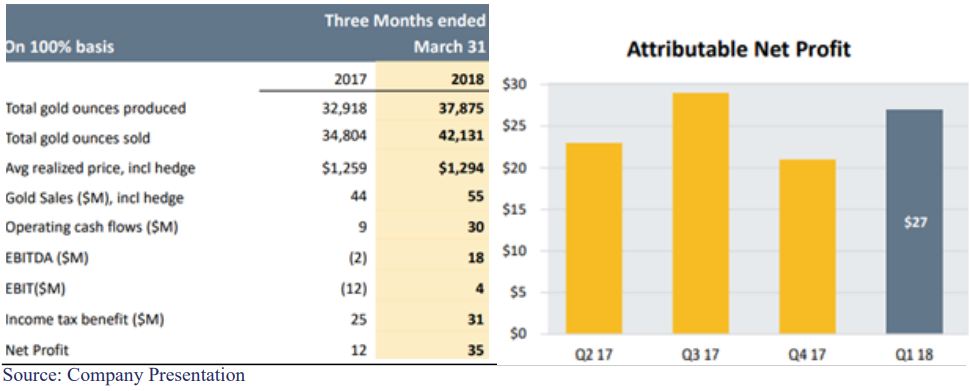

On May 1, the Company released its Q1 2018 financial results. Cash flow per share equated to $3.89. After these results the stock appreciated by 14.81%. The summary of the operational results and 2017 comparison are presented below.

Figure 4 & 5. Q1 2018 Financial Results Summary

Premier Gold Mines Ltd. (TSX:PG)

Premier Gold Mines is a gold producer with two mines located in Mexico and the U.S. The Company’s stock slipped 9% since our last report date, due to a negative Q4 2017 and lowered 2018 guidance.

The Company’s flagship mine is the Mercedes, an underground gold-silver mine located in the State of Sonora in northern Mexico. In 2017, the mine produced 83,000 oz Au. The mine’s 2018 production guidance is 80,000 – 85,000 oz Au with an AISC of US$820 – $870/oz Au. As of December 2017, the

mine has P&P reserves of 417,000 oz Au with an average grade of 3.94 g/t Au.

Premier holds a 40% interest in the South Arturo mine located in Carlin, Nevada. In 2017, the mine produced 57,124 oz Au and has a 2018 production guidance of 5,000 – 10,000 oz Au with an AISC of US$620 – $670/oz Au. The mine hosts a reserve of 270,000 oz Au with an average grade of 3.74

g/t Au. The Company aims to commence two open pit development projects for South Arturo in H2 2018. Through successful exploration in South Arturo in December 2017, P&P mineral reserves increased by 333% totalling 270,000 oz Au grading 3.18 g/t.

The Company’s 100% owned Cove property is an advanced exploration program in Nevada. The area was previously mined by Echo Bay Mines Ltd. from 1987 to 2001, and produced a total of 2.6M oz Au. Premier has a US$19M budget for the Preliminary Economic Assessment, to be released in H1 2018. The drilling and underground development is expected to commence in H2 2018, in advance of the Feasibility Study and deposit development, which is estimated to be completed in 2019 – 2020. The Company has two additional exploration properties located in Nevada and Ontario.

The Company also has a 50% share in the Greenstone Gold development project located in the city of Thunder Bay, Ontario. The project is anticipated to be completed in 2-4 years and is currently in its first phase, where the Company submitted their Environmental Assessment and Environmental Impact Statement for approval. Below is the summary of the 2016 Feasibility Study.

Figure 6. Feasibility Study

Source: Company Presentation

Source: Company PresentationGet Additional Ubika Research Reports on SmallCapPower.com Q4 2017 was $2.0M, a $5.8M reduction from the previous quarter’s net income. This decrease in net income is associated with the slight decrease in Mercedes gold production in Q3 and Q4 2017, as well as the slow down in production at South Arturo, due to the anticipated halt in mining for the Phase 2 underground extension. Within two days of the announcement, PG’s stock price dropped by 16.3% and by an additional 5% in the next week.

On April 10, the Company released high-grade gold results from exploration of its 100% owned Hasage Project in Ontario. The results showed 10m grading 8.5 g/t Au.

On April 17, the Company announced its Q1 production results. The South Arturo mine produced 15,000 oz Au, exceeding their higher range of the 2018 annual guidance. Mercedes gold production was slightly lower, due to their focus on developing new deposits.

On May 1, the Company release an update on the development of its South Arturo Mine. The highlights presented results from the El Nino area, which included 42.7m grading 11.2 g/t Au and 68.6 m grading 15.9 g/t Au. From its Phase 3 area results included 35.7m grading 16.5 g/t Au and 36.2m grading 8.0 g/t Au. After these results, the stock has appreciated by 5.4% thus far.

The Company has an average price target of $4.59, representing a 55% upside. The Company has 1 Strong Buy rating, 6 Buy ratings, 1 Hold rating, and no Sell ratings.

Upcoming Catalysts:

Continued geopolitical instability could be a catalyst for rising gold prices. Fears of trade wars, tensions with Iran and Russia, and continued Trump administration controversies could drive investors into non-U.S. assets.

First negative S&P 500 quarter since 2015 and an increasing U.S. budget deficit.The negative performance of the S&P 500 accompanied by an excessively large and growing U.S government debt can send bearish signals to investors. A recent J.P. Morgan survey demonstrated that three quarters of high net worth individuals are anticipating a U.S. recession in the next two years. Based on the low Gold to S&P 500 ratio, gold is currently considered to be undervalued and with an anticipated downturn, people might be adopting gold as a trustworthy store of valuepotentially reaching record levels of production.

Gold supply shrinking over recent years. In 2011, gold prices hit their peak and started to decline. Following the decline, explorers and producers reduced their costs by cutting their exploration budgets. With less deposit discoveries and lower gold mine output per year, there could be a potential supply.

To read our full disclosure, please click on the button below:

{kind=link}