Alex Cutulenco | Ubika Research Analyst | January 22, 2016: Canada’s Top 3 grocery chains sell nearly identical products, yet the similar ends when looking at long-term stock price performances. One has been devouring the competition, however our analysis shows this may not continue for long.

Alex Cutulenco | Ubika Research Analyst | January 22, 2016: Canada’s Top 3 grocery chains sell nearly identical products, yet the similar ends when looking at long-term stock price performances. One has been devouring the competition, however our analysis shows this may not continue for long.

The TSX and the S&P 500 are both down 8% year-to-date, as global oil prices, economic instabilities in China, and the rising USD (falling CAD) are adversely affecting the North American economy. When the economy worsens, consumers begin to get scared, which often time leads to reduced consumer expenditure, and a need for increased personal saving. Another insight we should remember, is that food (as in groceries) are a necessity (as opposed to a luxury good – such as fancy cars and restaurant expenses, which consumers are more inclined to forgive). Because of this, we would like to do a study on the top Canadian Grocers and depict why one particular Company is outperforming the other two by over 250%.

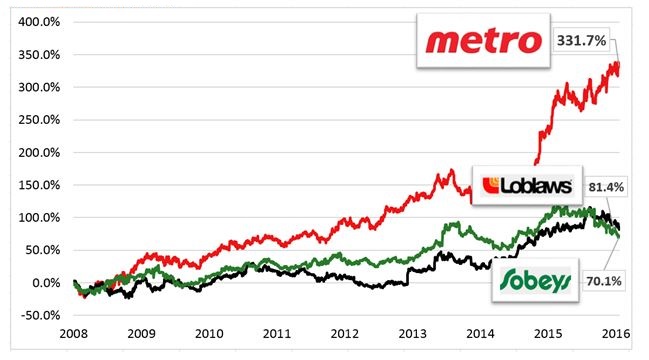

The chart below is frightening, that is if you falsely invested in either Loblaw or Sobeys.

Figure 1: Relative Return of Metro (TSX: MRU) vs. Loblaw (TSX: L) vs. Empire Companies (TSX: EMPa) since 2008

Source: Thomson Reuters (01/21/2016)

Source: Thomson Reuters (01/21/2016)

As you can tell, the relative performance is heavily skewed in one company’s favour: Metro Inc. knowing this, the natural instinct would be to check the financial performance of the group and see if the numbers add up.

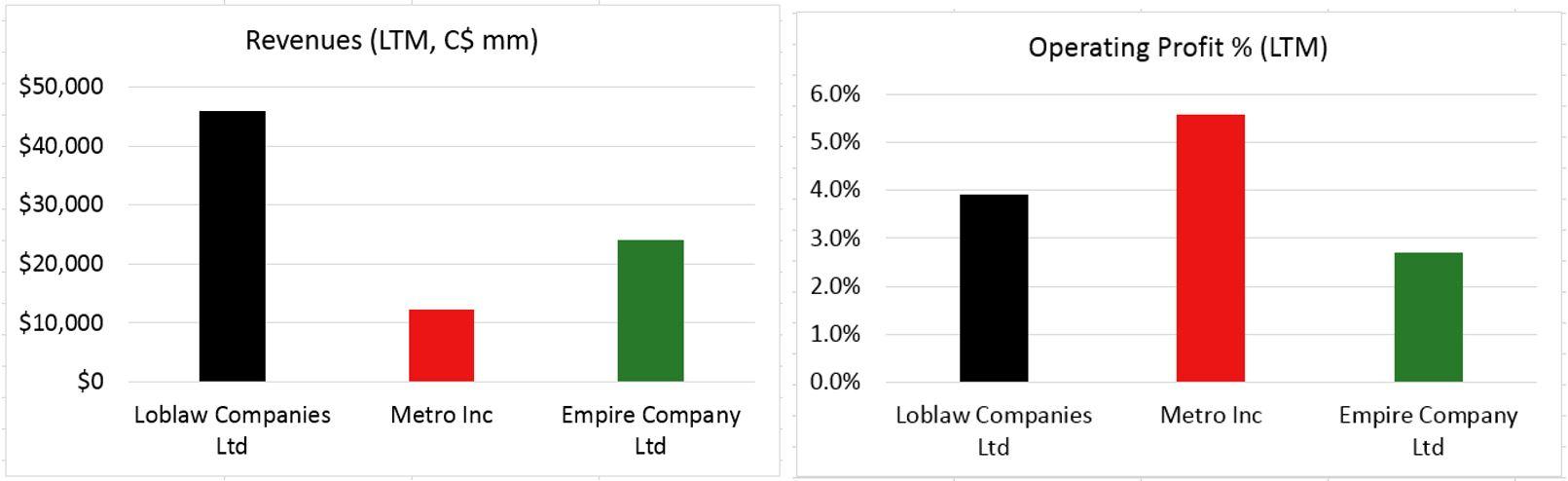

Operationally, Loblaw is by far the biggest of the group, with a Market Cap of $25 billion, and revenues of $46 billion. And although Metro, has the smallest share of revenues from the group, they post the largest operating profit margin (beating Loblaw by 1.7% – which is a dramatic difference in this low profitability industry where margins are crucially important).

Figure 2: Revenues vs. Operating Profit Margin (Last Twelve Months)

Source: Thomson Reuters (01/21/2016)

Source: Thomson Reuters (01/21/2016)

However, one thing that Metro is struggling with is growth. Metro posted a lackluster 1.5% Cumulative Average Growth Rate (CAGR) in Revenues over the last three-year period. This is pathetic compared to Loblaw’s 13.4% and Sobeys’ 12.4% growth. This of course gets translated onto the most important figure: Cash Flows. Free Cash Flow growth for Metro (over the last three fiscal years) was 11.2%, compared with 60.3% and 61.6% for Loblaw and Sobeys, respectively.

And yes, no Company can be good at every single business area (although generating revenue is a big part of the business), the analysis on whether any of these companies is a good investment will come down to valuation.

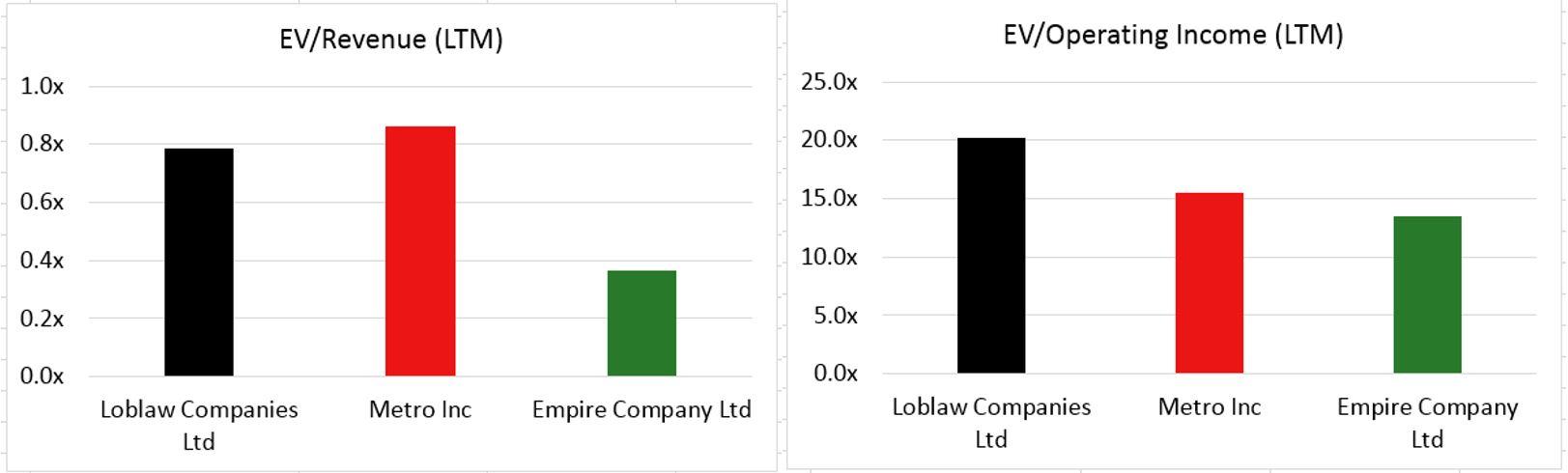

Figure 3: Enterprise Value Valuation Metrics

Source: Thomson Reuters (01/21/2016)

Source: Thomson Reuters (01/21/2016)

As can be seen from Figure 3, an unlikely candidate emerges: Empire Companies (i.e. Sobeys). Out of the group, they are relatively undervalued, and post impressive operational growth figures. Canada’s second-largest grocery chain continues to focus on expanding the footprint of its business through acquisitions (as can be remembered from its purchase of Canada Safeway in 2013, and Co-op Atlantic’s food and fuel business in Q1/2016), and yet the stock price took a nosedive from $32/share just under a year ago, to current $24/share.

With Metro’s upcoming earnings next week, investors should question the company’s ability to fuel growth, or whether the stock price has already appreciated enough. Maybe it will be Sobeys that experiences the next growth spurt?

Alex can be reach at: alex@gravitasfinancial.com

{kind=link}