Maven Mondays

What a start to the year. I am far from alone in noting it, but wow. I do get to say that things are playing out as I expected. I never pretended to know when or how the US would turn down, but I have been calling the US bull market tired and overdone for months already. But even though I saw markets with narrow breadth and earnings misses that had been relying on financial engineering and were starting to show topping patterns, it was impossible to know how the downturn would actually develop.

I do get to say that things are playing out as I expected. I never pretended to know when or how the US would turn down, but I have been calling the US bull market tired and overdone for months already. But even though I saw markets with narrow breadth and earnings misses that had been relying on financial engineering and were starting to show topping patterns, it was impossible to know how the downturn would actually develop.

Well, if 2016 continues the way it has started the downturn will be a crash. We are already in official correction territory: the S&P 500 is down 12% from its August high and the Dow Jones is down 13%. Small caps are faring far worse: the Russell 200 index of small caps is down 22%.

You don’t have to look back very far to see the last time this happened. In August US markets tumbled more than 10%. They recovered most of those losses, but the current slide means we’ve had two corrections in six months.

That has only happen three times in the last 100 years: in 1929, 2000, and 2008.

In a weak market gold shine as a safe haven; when a bull market ends investors search out sectors that still offer value, which mining does. I wanted the US to weaken to encourage investors to rotate into mining stocks, but I don’t want to see another Great Depression (1929), tech bubble fallout (2000), or Great Recession (2008)!

The next few days and weeks will be very interesting. If thing continue to weaken, the next question is whether a stock market correction or recession will depress the economy. Analysts are divided on the question.

I have said for a while that the weak US economy did not support a raging bull market. How much to credit the other way – how much the bull market helped the economy – is hard to know. Had stocks been rising because of real growth the relationship would have been clear, but instead the bull market was based largely in financial engineering (debt-fueled stock buybacks). If the bull turns bear it might drag on the US economy.

I would be just as worried, though, about impacts from a Europe struggling with a refugee crisis that is exposing the union’s weaknesses, about what a weakening Yuan will mean for the US dollar, and what oil’s plunge will mean for global market earnings, fund liquidations, and debt-driven bankruptcies (bond holders, beware).

I don’t like crowing about bad news (really!), but after Friday’s weak US industrial production numbers the Atlanta Fed updated its GDP Now assessment and pegged fourth quarter GDP at just 0.6%.

It all just points to weakness: in the markets, in the economy. Sucks for many investors and companies, but could well prove a boon for gold. The yellow metal is moving directly sideways today, a testament to how much it responds to US markets, which are closed today. That’s my note to start the week. Below, the In The News section of last week’s Maven Letter. There was lots to discuss. And as always, if you enjoy my writing consider signing up for a free trial subscription.

In The News…

Eldorado can’t wait any longer, suspends construction

Eldorado Gold is a textbook example of persistence. The company has excelled at getting mines built in challenging countries, but it seems it has met its match in Greece.

The company has been trying to develop its Kassandra mines in northern Greece since 2012, when it acquired European Goldfields. The Greek government approved the project’s environmental impact study in 2011, so Eldorado got to work building.

But “since 2012 the ministry and other agencies have not entirely fulfilled their permitting and licensing obligations.” They said yes to the mine, but in the face of protests from anti-mining groups they then just sat on their hands.

And the far-left Syriza government has been openly hostile to Eldorado. In 2015 the ministry revoked or suspended several permits. Eldorado took those decisions to court and won, but the company still lacks permission to build the process plant for one of the operations and to refurbish the mill that will serve the other mine.

As a result, Eldorado has now suspended work at Skouries, the mine that needs a mill permit, says it will suspend work at Olympias if the mill refurbishment permit is not granted soon, and is reconsidering whether to bother exploring for new reserves at its operating Stratoni mine, where ore will run out in three years without new work.

The company is stuck. It cannot continue to develop its mines without certainty that it will be able to build mills. Since 2012 the company has spent US$700 million at Kassandra. Eldorado says it has “the support of the vast majority of the local stakeholders,” suggesting opposition is driven by external anti-mining groups. It has tried to take the legal road and has won numerous decisions from Greece’s Supreme Court confirming the integrity of its permits, which represent a contractual obligation for the Greek State to finish the job. But none of it has helped.

Political risk is such a bugger. How can you win when your opponent controls the country? External observers point out that Greece needs all the jobs and investment it can get, but that doesn’t stop anti-mining activists.

Eldorado will survive. Greece is just one part of ELD’s portfolio of operations, which includes three gold mines in China, two gold mines in Turkey, and exploration/development assets in Romania and Brazil. Its share price still took a big hit on the news, falling 24%, and several analysts cut their target prices.

Rubicon: This Phoenix Ain’t Rising

The saga that is Rubicon Minerals continues. The stock, worth $6.50 in 2010 and as much as $1.63 at the start of 2015, is now worth just $0.03.

The story is a lesson in assumptions.

Rubicon decided to turn its Phoenix discovery into an underground gold mine based on a preliminary economic assessment. PEAs are the first step in planning a mine but they should be followed by a feasibility study, a far more intensive process including higher standards for geologic data, construction-ready engineering plans, comprehensive metallurgy, and detailed mine planning.Rubicon skipped that step. The result: a failed mine.

A year ago a list of stock pickers and analysts tagged Rubicon as the opportunity of the year, an undervalued stock set to be re-rated as soon as Phoenix reached production. Those predictions trembled some as costs crept up, but things still appeared ok until early October when RMX suspended milling because of environmental concerns raised by the Ontario government. The same day, company president Michael Lalonde stepped down.

When the guy who took the project from paper to production steps down before achieving success, there is more amiss than ammonia levels in the tailings.

A month later the real story surfaced when Rubicon halted mining to “enhance its geological model”. In other words, Rubicon had to figure out how to mine a deposit that was way more complicated close up than its models had predicted.

Now the final dagger: after revising the gold count down by 88%, Rubicon has stopped even trying to figure out how to mine Phoenix.

I say the story is a lesson in assumptions, but I don’t mean to say the mistakes here were obvious. Drilling, metallurgical work, engineering, and modeling are slow, boring, and costly endeavors. It is natural to want to speed instead to production, to cash flow and success.

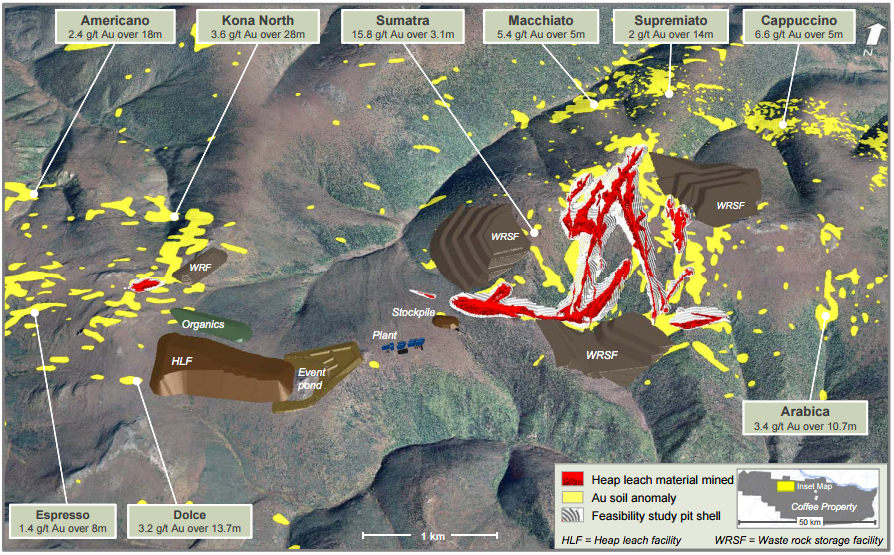

What Rubicon really represents is a lesson in caution. If a project seems too good to be true, it probably is. A good comparison here is Kaminak, advancing the Coffee project in Yukon. As an open pit, heap leach operation, Coffee is a much simpler project than Phoenix, where an underground mine had to accurately mine and efficiently recover very nugget-y gold.

Despite the relative simplicity, Kaminak just spent 18 months preparing a feasibility study. Now it will focus on permitting. These are ‘boring’ days for Coffee – but if the project does become a mine, the work being put in today greatly improves its odds of success.

Rubicon is now trading at half its bank balance. I still wouldn’t touch it, since debts and closure costs far exceed that $22 million.

Are Royalty Companies Telling Us Something?

Royalty companies have been spending big. The top three royalty firms committed $3.8 billion in the second half of 2015, a massive level of investment from a sector many like to call the ‘smart money’ in mining.

The royalty sector is still pretty young, so while I don’t dispute that they have outshone miners dramatically over the last decade I would also point out that they haven’t had as long to make mistakes. And mistakes they will make (royalty firm Royal Gold signed a US$75-million streaming deal on the failed Phoenix project, for example).

But the entire structure of the royalty business put the odds in their favour. Since they do not explore or build mines, their technical teams focus 100% on stress testing projects of interest to ensure they make investment sense while their capital markets teams focus on figuring out the best time to ink each deal.

Apparently those groups are collectively figuring the time is now. To me, that means these teams think we are at the bottom.

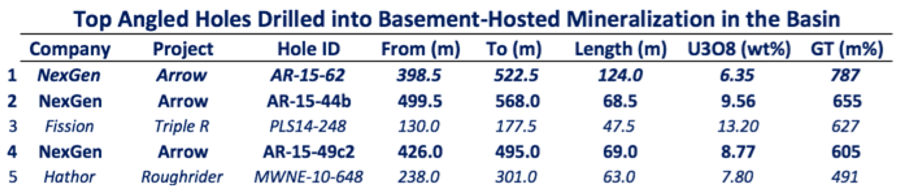

NexGen reports the best basement-hosted uranium intercept ever from the Athabasca

NexGen reported the final hole of its summer 2015 program and it is stunning.

78 metres grading 10% U3O8

It is difficult to emphasize how impressive that intercept is. For starters, remember that mines in the Athabasca Basin tap into the highest-grade uranium in the world, with ore averaging 100 times the global average. And NexGen’s latest hole is the best hole ever pulled from basement-hosted Athabasca mineralization.

Now the Athabasca offers two kinds of uranium – unconformity/sandstone hosted and basement hosted. And unconformity/sandstone deposits have also produced some stunning hits. Nevertheless, hole 62 is one for the record books.

The hole usurps hole 44b as the best hit from Arrow to date. It was drilled 22 metres updip from that stunner (68.5 metres grading 9.56% U3O8) and as such emphasizes that the intense mineralization in the high-grade A2 subzone is nicely continuous.

Hole 62 is also the last drill result that will feed into NexGen’s maiden resource estimate for Arrow, which I expect will impress.

Cantor Fitzgerald analyst Rob Chang’s comments help capture the significance of this result.

“These are the types of assay results that people talk about for years. It is among the best we have ever seen across any commodity, as evidenced by the fact that its gold-equivalent numbers translate into 219 g/t gold equivalent over 78 metres. On its own, we estimate that this hole represents 9.7 million lbs. U3O8.”

Two days earlier NexGen released results from three other holes. That set included the best hole drilled to date in the A3 shear: hole 61c2 returned 10.5 metres of 8.52% U3O8 followed by 37 metres of 6.3% U3O8.

Those are also very impressive numbers. Most excitingly, they suggest that A3 might host a high-grade core similar to that in A2.

In addition, hole 59c3 cut 4.5 metres of 13.17% U3O8 from the southwest edge of A3. That bodes well for expanding this shear to the southwest, which is one of NexGen’s goals in the current winter program.

A round of applause for Kaminak’s feasibility

It has been a week since Kaminak released its Coffee project feasibility study and sifting through analyst reports and market feedback I have seen nothing but positive response. I agree. The study achieved or surpassed all of its stated goals while using conservative assumptions, and left room for improvement.

Let’s focus on the changes.

- Output is higher and mine life is shorter. The new plan has Coffee producing an average of 194,000 oz. annually for 10 years, up from 167,000 oz. per year over 11 years.

- Operating costs are lower because the new plan uses 2-stage crushing to generate 2-inch feed, versus 3-stage crushing to 0.5-inch. Extensive metallurgical testing shows recoveries are only minimally lower from the larger feed.

- Feed grade is now 1.45 g/t gold, up from 1.23 g/t gold previously, primarily because of infill drilling and improved deposit modeling.

- Capital costs are down because the leach pad has changed from a valley-fill facility (requiring an extensive liner and a big dam) to a ridge-top design, which is more straightforward to build, and because the new road plan requires considerably less new build.

The feasibility outlines a better mine than did the PEA, with lower costs, and it was all completed in 18 months. That is impressive.

There remain several ways the plan could improve from here:

- Buying secondhand equipment for the mill and the mining fleet, which should be readily available in this depressed market.

- Reserve growth. This is the biggie. At present only 2.2 million ounces of Coffee’s 5.2 million ounce resource are included in the mine plan. If the gold price strengthens, pits would expand to include more ounces and those ounces would boost Coffee’s economics. Haywood’s model, for example, has Coffee offering an additional $0.30 in net asset value per share for every US$50 per oz. increase in the price of gold.

- On top of that, Kaminak has focused on getting this project through feasibility, which means drilling has been primarily infill for the last 18 months. But the property still offers extensive gold-in-soil anomalies that are untested or minimally tested.

KAM shares enjoyed a nice run up before the feasibility study came out (the company had promised, repeatedly, that the study would land early in the new year). They have since settled some. Kaminak, with one of the best development-ready gold assets in the world, remains a buy at these levels.

{kind=link}