This cannabis investing special report will examine the current state of the cannabis industry and seek to address the potential and risks of the industry after recreational legalization in Canada

SmallCapPower | October 17, 2018: In Canada, rumours of recreational cannabis legalization started circulating in 2017 and immediately caught the interest of investors, and for good reason. Back in January, Statistics Canada estimated that Canadians spent $5.7 Billion on cannabis products in 2017, 90% of which was illegally produced and sold. Consequently, the legalization of recreational cannabis offers a ‘once in a lifetime’ opportunity through access to a multi-billion-dollar market. Over the past year, HMMJ (the TSX-listed cannabis Exchange Traded Fund) has experienced extreme price fluctuations that underlines investor uncertainty surrounding the sector. From October 1, 2017 to January 9, 2018, HMMJ increased 135% peaking at $24.33. Then a market correction occurred in January causing HMMJ to drop by 33% to $16.45 by February 2, 2018. Following the correction, Canadian cannabis stocks leveled off, but following the announcement of formal recreational legalization by the Canadian Prime Minister Trudeau on June 20, interest in cannabis investing has reached an apex. Since August 14, HMMJ has climbed 75%, reaching an all-time high of $26.50 on October 16, 2018.

This report will examine the current state of the cannabis industry and seek to address the potential and risks of the industry after recreational legalization. We selected Aphria Inc. (TSX:APH) as a case study to assess current valuations, product diversity, and operations strategy.

Upcoming Conferences

MJBizCon – Las Vegas Convention Centre, Las Vegas, Nevada, November 14-16, 2018. MJBizCon is the largest cannabis conference in the world.

The Science of Cannabis

The cannabis plant can be grown from many different strains including hemp and marijuana. Each strain is differentiated by its chemical composition of cannabinoids and terpenes that give the plant its unique dose, tolerance, and effects when consumed.

Cannabinoids

There are over 100 different cannabinoids (chemical compounds) present in cannabis, but the two main types that are cannabidiol (CBD) and tetrahydrocannabinol (THC). THC is the active compound in recreational cannabis, well-known for its psychoactive effects, giving the user a ‘high’ sensation. Some of the effects of metabolized THC include relaxation, euphoria and increased appetite but anxiety and paranoia can be side effects in extreme cases. CBD, on the other hand, is commonly used in the medical profession due to the lack of psychoactive effects and instead has been used to treat anxiety, inflammation, pain, and select forms of epilepsy. In the cosmetics industry, CBD oil has been popularly utilized in the creation of mascaras, face creams, and lip-balms as a vegan alternative to beeswax.

Depending on the intended function, there are many strains with high CBD or THC potencies, or a combination of both at many varying levels, which is known as a hybrid strain.

Industrial Use of Cannabis

Outside of its chemical compounds, cannabis has been utilized by the industrial sector for decades. Due to its fast-growing nature, cannabis can be efficiently cultivated and woven into hemp fibers to be used in the manufacturing of textiles, paper, biodegradable plastics and insulation. This means that cannabis has effectively three commercial uses; recreational, industrial, and medical. It is important for investors to understand all the commercial uses of cannabis and not be limited to the potential of recreational cannabis sales. A shrewd investor will acknowledge that cannabis has multiple revenue streams and will identify companies with the resources to best service each of these industries.

Highlighted Company: Aphria Inc. (TSX:APH)

Company Overview

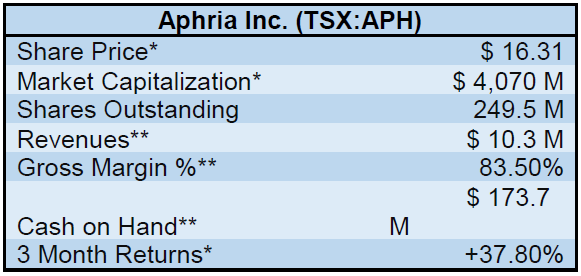

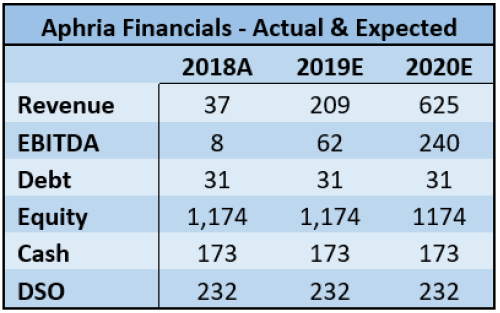

Headquartered in Leamington, Ontario, Aphria is the third-largest cannabis company by market capitalization listed on a Canadian stock exchange, behind Canopy Growth Corp. (TSX:WEED) and Aurora Cannabis (TSX:ACB). Aphria is a licensed producer (LP), cultivating and selling a range of medical cannabis-based products both in Canada and internationally, including flowers, gel capsules, concentrates, edibles and topical creams. Through a series of acquisitions and organic growth, Aphria manages a portfolio of several premium and recreational brands including Broken Coast and Solei. Figure 1 below summarizes key financial information about the company.

Figure 1: Aphria Key Financial Information, in Canadian Dollars.

*As of Oct 5, 2018. ** As of Q3 2018 Source: Capital IQ, Ubika Research

*As of Oct 5, 2018. ** As of Q3 2018 Source: Capital IQ, Ubika Research Business Operations

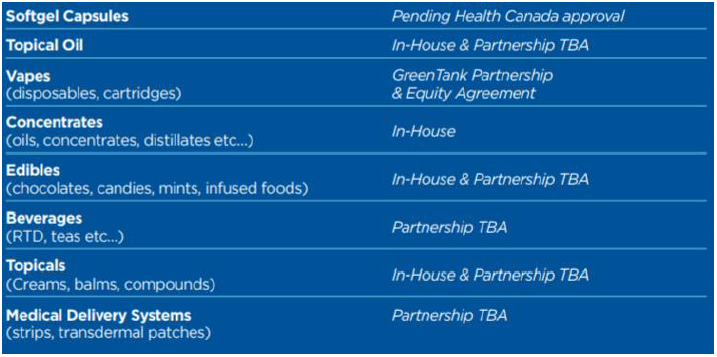

Aphria Inc. has strategically positioned itself within the industry by developing a breadth of product offerings that extend beyond just the traditional flower-based cannabis products. These products include oils, concentrates and edibles. As shown in Figure 2, the Company has made significant efforts in growing its brand portfolio, with each brand meeting specific consumer needs, differing in price points and product formats to appeal to a broader audience. On September 28, 2018, Aphria announced the first brands available for sale upon legalization: Solei, RIFF, Good Supply, Goodfields, and Broken Coast. Each brand is differentiated to appeal to a specific audience. For example, the Broken Coast brand delivers a premium experience using cannabis grown on the Salish Seas in British Columbia. Meanwhile, Good Supply is a brand targeted at value-conscious consumers looking for an everyday experience. Figure 3 depicts the Company’s brand portfolio.

Figure 2: Planned Product Offerings

Source: Company Presentation

Source: Company PresentationFigure 3: Brand Portfolio

Source: Company Presentation

Source: Company PresentationAs the Company prepares for recreational legalization, it plans to cut wholesales deliveries to other LPs to build up its inventories. This will likely reduce revenues in Q4 2018, but it should provide favourable financial results once the higher recreational sales are captured and reported in early 2019.

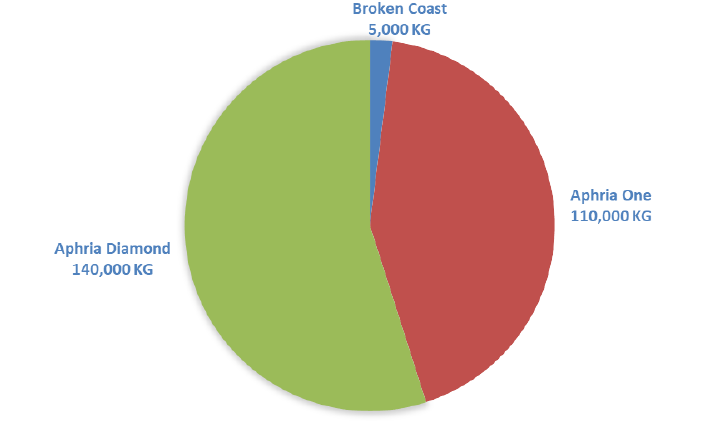

Aphria’s production capacity as of July 2018 totaled nearly 35,000 kg, with plans to significantly ramp up production leading up to January 2019, when it expects production to exceed 250,000 kg on an annualized basis. Aphria currently has three major expansion projects: Aphria One, Aphria Diamond, and Broken Coast. The Aphria One project, when completed, will provide the Company with a 700,000 square foot facility, with first sales expected in early 2019. Aphria Diamond has applied for a cultivation license, while recent investments in the facility is expected to support alternative growing techniques. Lastly, Broken Coast, a wholly-owned subsidiary of Aphria, operates an indoor facility on Vancouver Island, producing products marketed under the premium Broken Coast brand. Figure 4 illustrates the Company’s planned production capacity for January 2019.

Figure 4: Expected Production Capacity as of January 2019.

Source: Ubika Research, Aphria Presentation

Source: Ubika Research, Aphria PresentationThrough a series of acquisitions and strategic partnerships, Aphria has been able to expand to establish an international presence. Notable acquisitions and partnerships include partial ownership of the Australian LP Althea, and the acquisition of LATAM Holdings in Latin America. Aphria owns a 37.5% equity stake in Althea, a licensed importer and producer of medical cannabis in Australia. In April 2018, the Company completed its first shipment of branded cannabis oil and dried flower products for sale in the Australian market, in partnership with Althea.

Aphria also made shipments of high CBD and THC cannabis oil products to Medlab Clinical Limited of Australia, as part of a supply agreement dating back to April 2017.

On September 27, 2018, Aphria announced the closing of its acquisition of LATAM Holdings, establishing the Company’s presence in Latin American and Caribbean countries including Columbia, Argentina, Jamaica, and potentially Brazil. The climate of Central/South America makes for ideal growing conditions allowing for low cost of production for both local and export uses, further solidifying Aphria’s reputation as a low-cost producer. Figure 5 below illustrates the Company’s international expansion initiatives.

Figure 5: Aphria International Expansion Strategy

Source: Company Presentation

Source: Company PresentationSupply Agreements

Supply agreements ensure stable cash flows in a world of ever-increasing supply. These agreements allow producers to lock in a predetermined amount of product to be supplied at a specific price. In addition to allowing for steady, predicable revenue streams and distribution agreements can also act as a hedge against fluctuations in demand and supply. If supply were to dramatically outpace demand, for example, an agreement would ensure incoming cash flows, whereas a company without an agreement could struggle to sell product. As such, Aphria has entered into several recreational supply agreements to ensure it captures a sizable share of the market post legalization. Below are some key agreements for Aphria:

- Ontario: To supply 59 SKUs to Ontario Cannabis Store for online sales

- Quebec: 12,000 kg per year

- British Columbia: >5,000 kg per year

- Manitoba: 2,700 kg per year

- Shoppers Drug Mart: Pending Health Canada’s approval, to be sold directly to consumers online.

On September 7, 2018, Aphria announced a supply agreement with Auxly Cannabis Group (TSXV:XLY), allowing Auxly to purchase up to 20,000 kg of cannabis products from Aphria on an annual basis until January 31, 2022, when the agreement can be renewed. Auxly distributes cannabis products to international markets including Mexico, Portugal, and Serbia.

More recently, on September 12, 2018, the Company announced an LP-to-LP supply agreement with Emblem Corporation (TSXV:EMC). The agreement commits Emblem to an aggregate of 175,000 kg equivalents of cannabis-based products from Aphria over a five-year period. Emblem posted an initial deposit of $12M in cash and issued nearly seven million common shares, giving Aphria a 5.5% equity stake in Emblem.

Performance

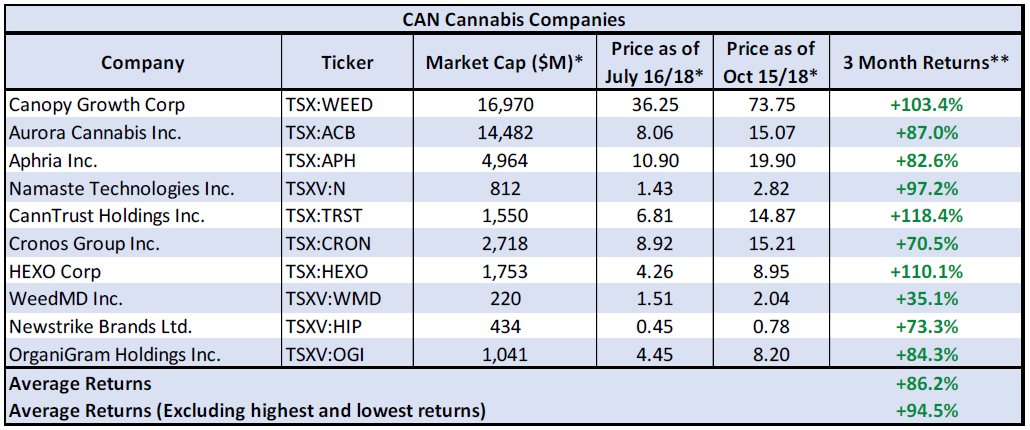

Figure 6 outlines the price performance of Aphria over the past three months as compared to other Canadian cannabis stocks in the industry.

Figure 6: Price Performance of Canadian Cannabis Companies (Last 3 Months)

*Market Cap and Price Data as of Oct 15, 2018. All figures are in Canadian Dollars.

*Market Cap and Price Data as of Oct 15, 2018. All figures are in Canadian Dollars.**Returns for the period July 16, 2018 to October 16, 2018

Source: Capital IQ

Valuation

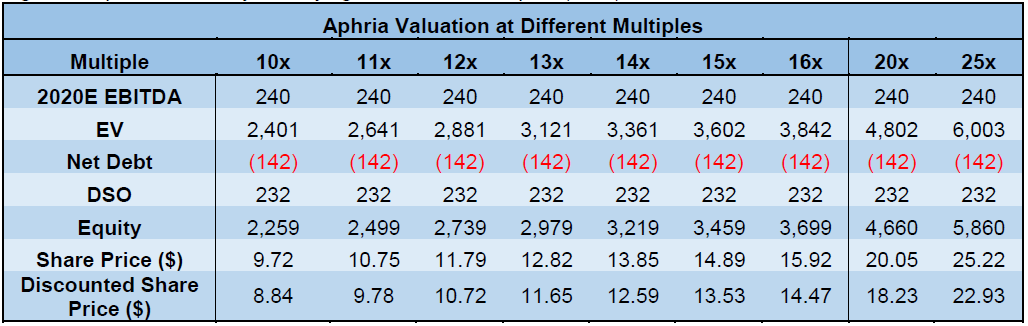

To properly value a cannabis company such as Aphria, we must look at the projected cash flows generated post-legalization. We have valued Aphria using a multiples approach using consensus 2020E EBITDA for our sensitivity table. Aphria is currently valued at a ~20x forward (2020) EV/EBITDA multiple (share price as at October 9: $17.42). For comparison, the alcoholic beverage industry commands multiples of 10x EV/EBITDA, while average tobacco industry multiples are closer to 16x EV/EBITDA.

Figure 7: Aphria Financials (CAD)

Source: Ubika Research, Capital IQ

Source: Ubika Research, Capital IQFigure 8: Aphria Sensitivity at Varying EV/EBITDA Multiples (CAD)

Source: Ubika Research, Capital IQ

Source: Ubika Research, Capital IQ*Used a discount rate of 10%

Canadian Private Retail Distribution

During 2018, many licensed cannabis producers, Aphria included, made strategic acquisitions or partnerships to become a true ‘seed-to-sale’ (vertically-integrated) company. Seed-to-sale refers to a company’s involvement in the entire product journey: from cultivation, to refining products, distribution to retailers and finally the sale of product to the consumer.

However, plans for producers to establish vast retail distribution in Ontario came to an abrupt halt when the provincial government announced that each LP would be limited to one retail location within the province. Considering that Ontario accounts for ~38% of the 36 million Canadian population, this represents a significant loss for LPs looking to capture significant market share through diverse brick and mortar retail distribution. Instead, independent retailers will be given the power to pick and choose which brands they want to carry. Meanwhile, online retail within Ontario will be regulated by the ‘Ontario Cannabis Store’, making it difficult for producers to differentiate themselves from competitors.

The news doesn’t get much better outside of Ontario, as Quebec (23% of population) is restricting cannabis sales to its government-run alcohol agency. Similar for British Columbia (13%), which is expected to utilize its Liquor Distribution Branch to operate wholesale cannabis distribution and government-run retail stores. On the other hand, Alberta (12%) might offer the best scenario, as the province is anticipated to allow single LPs to operate private retail locations to a maximum of 15% of available market.

Legalization of Edibles

While recreational cannabis is set for legalization on October 17, 2018, it will be limited to ‘bud’ and oil-based cannabis products. Edible cannabis products make up a significant amount total cannabis revenue. According to Forbes magazine, the edibles market was worth US$7.2 billion in the United States in 2016. Furthermore, a study conducted by Deloitte showed considerable interest in the cannabis edibles market even though edible cannabis products will not be available until October 2019. Of the 1,500 people surveyed, 60% of ‘likely’ cannabis consumers are expected to prefer edible products.

However, the year delay in edible legalization has not prevented LPs from making significant investments in producing edible cannabis products, ranging from cake mix to beverages. Most notable was the $4B investment by Constellation Brands (NYSE:STZ) into Canopy Growth Corp (TSX:WEED) to fuel global expansion, but also to develop cannabis-based beverages. For investors, it is important to realize that revenues from edible cannabis sales will not be realized until at least a year and a half from now. The earliest possible date for legalization of edible cannabis is October 2019.

Legalization of Cannabis in the United States

The road to cannabis legalization in the United States has been anything but linear. Cannabis has been classified as a Schedule I substance since 1970 making it illegal for possession under federal law. However, the Rohrabacher-Blumenauer amendment, passed in 2014, prevents the Department of Justice from prosecuting cannabis-related activities if the individual is permitted under state law. The amendment gives autonomy to each U.S. State to form their own policies regarding cannabis legalization. To date, 31 states have legalized marijuana for medical use and nine states have legalized cannabis for recreational use. States that have legalized cannabis for recreational use include: California, Colorado, Maine, Massachusetts, Nevada, Oregon, Vermont, Washington and Alaska.

Although the legalization of recreational cannabis (on the federal level) remains uncertain, U.S. based cannabis producers can still offer significant upside for investors. The State of California has a larger market than the entirety of Canada, boasting a population ~40 million. However, because state borders are federally regulated, U.S. cannabis cultivators are unable to legally transport cannabis across state lines. Therefore, cannabis production in California is limited for sale within the state with any excess production being written off as a sunk cost.

The Controlled Substances Act includes Hemp-based CBD as Schedule I substance making it federally illegal along with marijuana. However, the Hemp Farming Act, introduced to Congress back in May, would legalize hemp-based CBD products and open the U.S. market to medical cannabis products. This would represent a significant opportunity as The Brightfield Group estimates the market for CBD products within the United States could be as high as $22 billion. Although medicinal marijuana is already legalized at the state level in 31 locations, legalization at the would allow for interstate sales and distribution opportunities. The Hemp Farming Act is expected to pass through Congress later this year and is a key topic for investors to track in the coming months, although the FDA would still have to approval hemp for consumption in the United States.

Industry Consolidation

According to Capital IQ, there are currently 107 publicly-traded cannabis companies operating in Canada with a market capitalization greater than $10M. Following legalization, demand for cannabis products is expected to be high and there are some concerns that current supply will not meet the demand, as many of the major producers in Canada are undergoing major plant expansion projects that are not due to be completed until 2019. It is expected that supply deals, such as the one between Aphria and Emblem Corp, will help curb the supply issue. We also believe that competitor consolidation will happen as LPs acquire competitors with key regional footholds to capture further market share. Additionally, the fierce competition will inevitably force cannabis producers with inferior cost control, product and branding out of the market. We expect that the competitive landscape in the Canadian cannabis industry will look drastically different in the next five years.

To read our full disclosure, please click on the button below:

{kind=link}